EXCITING NEWS: TNG WhatsApp Channel is LIVE…

Subscribe for FREE to get LIVE NEWS UPDATE. Click here to subscribe!

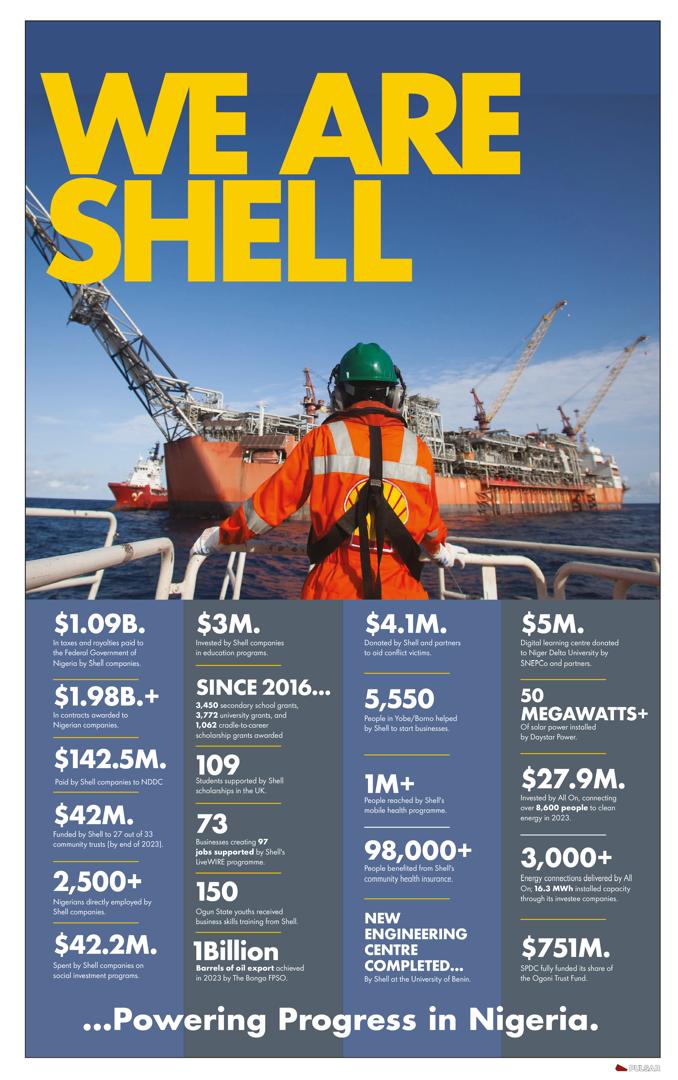

The growth recovery in Nigeria for 2023 is still fragile as oil production remains subdued and the new administration faces many policy challenges.

Advertisement

A new world bank report has revealed that Sub-Saharan Africa faces a myriad of challenges to regain its growth momentum, including the protracted slowdown of growth of investment in the region, which limits its efforts to reduce extreme poverty and boost shared prosperity in the medium to long term.

The April 2023 edition of the World Bank Africa’s Pulse data report showed that growth across Sub-Saharan Africa remained sluggish as a result of “uncertainty in the global economy, the underperformance of the continent’s largest economies, high inflation, and a sharp deceleration of investment growth”.

This outlook poses challenges to policy makers in the region who seek to accelerate the post-pandemic recovery, reduce poverty, and put the economy on a sustainable growth path.

Economic growth slowed to 3.6 per cent in 2022, from 4.1 per cent in 2021 and economic activity in the region is projected to further slow down to 3.1 per cent in 2023, a 0.4 percentage point downward revision compared to the October 2022 Africa’s Pulse forecast.

“Growth is estimated to pick up to 3.7 and 3.9 per cent in 2024 and 2025, respectively – thus signalling that the slowdown in growth should be bottoming out this year,” the report said.

A rebound of global growth later this year, easing of austerity measures, and more accommodative monetary policy amid falling inflation are the main factors contributing to the increased growth along the forecast horizon.

The report noted that the growth recovery in Nigeria for 2023 (2.8 per cent) was still fragile as oil production remained subdued and the new administration faces many policy challenges.

Inflation remains persistently high and above target and will continue to weigh on economic activity; consumer price inflation in Sub-Saharan Africa accelerated sharply and hit a 14-year record high in 2022 (9.2 per cent), fueled by rising food and energy prices as well as weaker currencies.

Climate shocks, especially in the Horn of Africa, add inflationary pressures from the supply side and the number of countries with two-digit average annual rates of inflation increased from 9 in 2021 to 21 in 2022.

Public debt in Sub-Saharan Africa has more than tripled since 2010, with a sharp increase prior to the onset of the COVID-19 crisis.

According to the report, the surge in public debt has been accompanied by a shift in its composition toward domestic debt—particularly, to meet pandemic-related financing needs and domestic debt accounted for nearly half of the outstanding public debt by the end of 2021.

“Fiscal dominance and foreign exchange rate restrictions may lead to inflation outcomes that are contrary to what monetary tightening intends.

“In Sub-Saharan Africa, curbing inflation remains essential to boost people’s incomes and reduce uncertainty around consumption and investment plans,” the report said.

Therefore, it recommended that policies to fight against inflation should be complemented by income support measures (via cash or food transfers) to protect the most vulnerable from stubbornly high inflation—particularly, food inflation.

It added that African governments must sharpen their focus on macroeconomic stability, domestic revenue mobilisation, debt reduction, and productive investments in the face of dampened growth prospects and rising debt levels.

“In a time of energy transition and rising demand for metals and minerals, resource-rich governments have an opportunity to better leverage natural resources to finance their public programs, diversify their economy, and expand energy access.

“Africa’s natural resource wealth holds significant untapped economic potential. About one-third of the total stock of wealth in Sub-Saharan Africa is held in various forms of natural capital, including renewable natural capital like cropland, water resources, and forests, as well as nonrenewable subsoil assets.”

The region’s nonrenewable petroleum and mineral deposits reached more than US$5 trillion in value during the boom years (2004–14) and Sub-Saharan Africa has seen more major petroleum discoveries since 2000 than any other region in the world.

![[Devotional] IN HIS PRESENCE: Increase comes from God](https://thenewsguru.com/wp-content/uploads/2023/02/Screenshot-2023-02-21-at-5.48.27-AM-75x75.png)

{kind=link}